A shipment leaves the warehouse on schedule. The purchase order was large, the relationship with the distributor is well established, and the credit terms are standard—net 60 days.

For years, the arrangement has worked smoothly. But economic conditions begin to shift. Demand softens in the distributor’s market. Inventory starts moving more slowly. Cash flow becomes tighter.

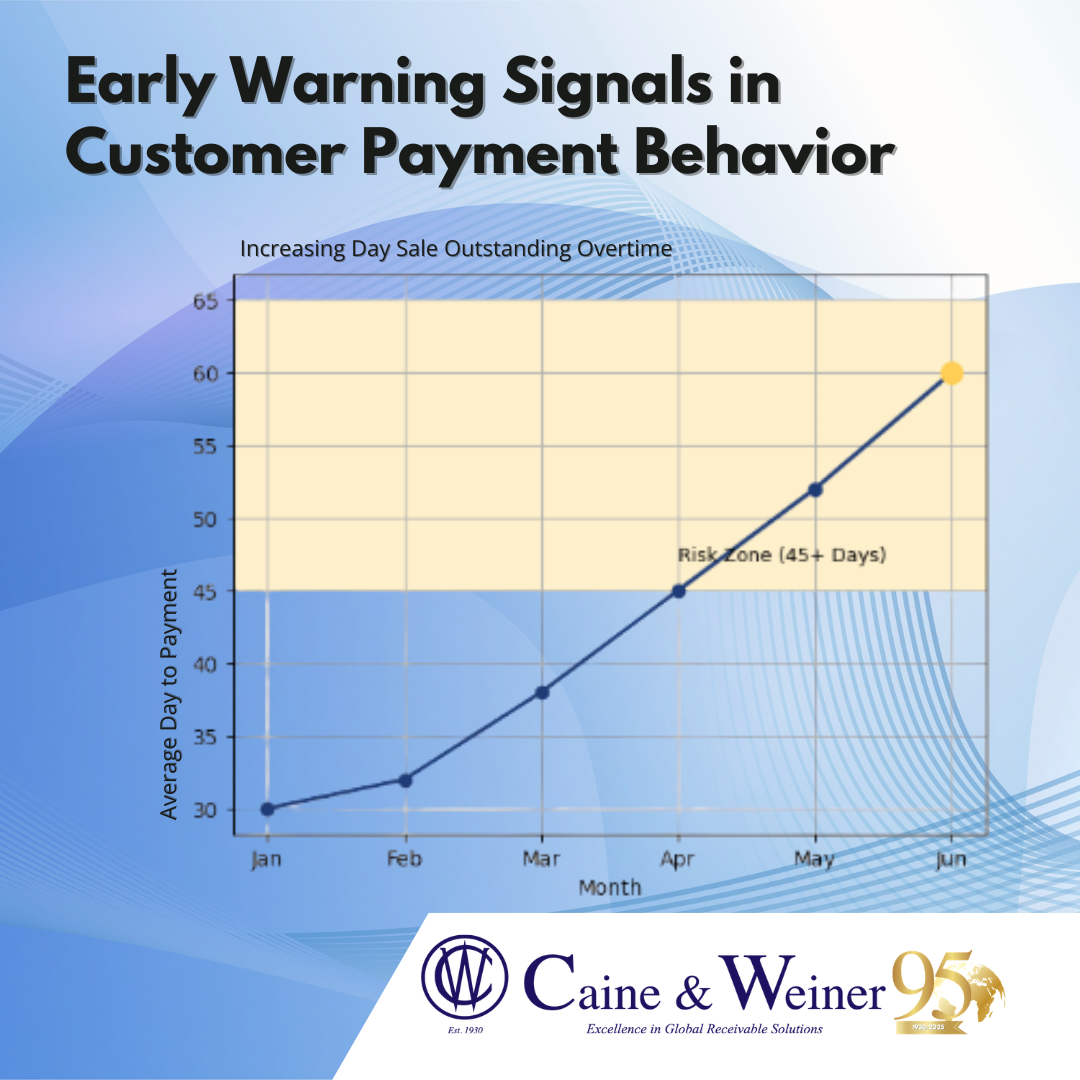

The invoice remains unpaid longer than usual. Situations like this illustrate a reality many manufacturers face: credit risk doesn’t exist only in financial reports. It exists throughout the supply chain, including directly on the factory floor.

Manufacturers frequently extend substantial trade credit to customers. This practice supports long-term partnerships and enables large-scale distribution networks to operate efficiently.

However, every credit line represents exposure. When customers experience financial pressure, suppliers are often among the first to feel the impact.

Unlike banks or traditional lenders, manufacturers may have limited visibility into a customer’s broader financial health. Payment patterns often provide the earliest warning signals that risk is increasing.

A customer who consistently paid within 30 days may begin drifting toward 45 or 60. Communication may become less frequent. Partial payments may appear. These subtle changes can indicate growing financial stress.

Monitoring payment trends closely allows finance teams to identify these signals before balances escalate. Credit management strategies play an essential role in protecting manufacturers from excessive exposure.

Regularly reviewing customer payment histories helps identify accounts that may require closer oversight. Adjusting credit limits based on updated financial information can reduce potential losses if conditions deteriorate.

Diversifying customer portfolios also helps mitigate risk. Relying heavily on a small number of large buyers can amplify financial vulnerability if one account encounters difficulty.

Proactive communication is equally important.

Many payment issues can be resolved through early dialogue. Customers experiencing temporary challenges may be willing to establish structured repayment plans or modified payment schedules.

These arrangements help maintain the business relationship while preventing accounts from aging into delinquency. In today’s economic environment, manufacturers operate in an interconnected financial ecosystem. Payment behavior in one segment of the supply chain can quickly influence liquidity throughout the entire network.

Credit management, therefore, is not simply a financial safeguard—it is a strategic component of operational stability.

Because on the factory floor, production efficiency keeps goods moving. But disciplined credit oversight ensures that revenue follows.