Banking and commercial real estate (CRE) have always been interconnected. When CRE performs well, banks enjoy predictable income streams, stable deposits, and manageable risk exposures. But when CRE weakens—banks feel it first, and they feel it hard.

Today, that pressure is reaching a critical point.

Office vacancies remain historically high. The shift to hybrid work continues to reduce demand. Maturing loans face refinancing at significantly higher interest rates. And delinquency cycles, once contained within specific pockets, are beginning to spread across retail, industrial, and even multifamily sectors.

The result? Rising CRE delinquencies are now testing banks’ reserve lines, squeezing liquidity, and elevating credit risk to levels not seen in over a decade.

Caine & Weiner’s long-standing partnerships across financial institutions have provided deep visibility into the shifting 2025 credit landscape. And the message is clear:

Banks must strengthen receivables oversight, modernize collection strategies, and adopt more proactive loan management—before CRE stress impacts capital requirements.

The CRE Market in 2025: A System Under Strain

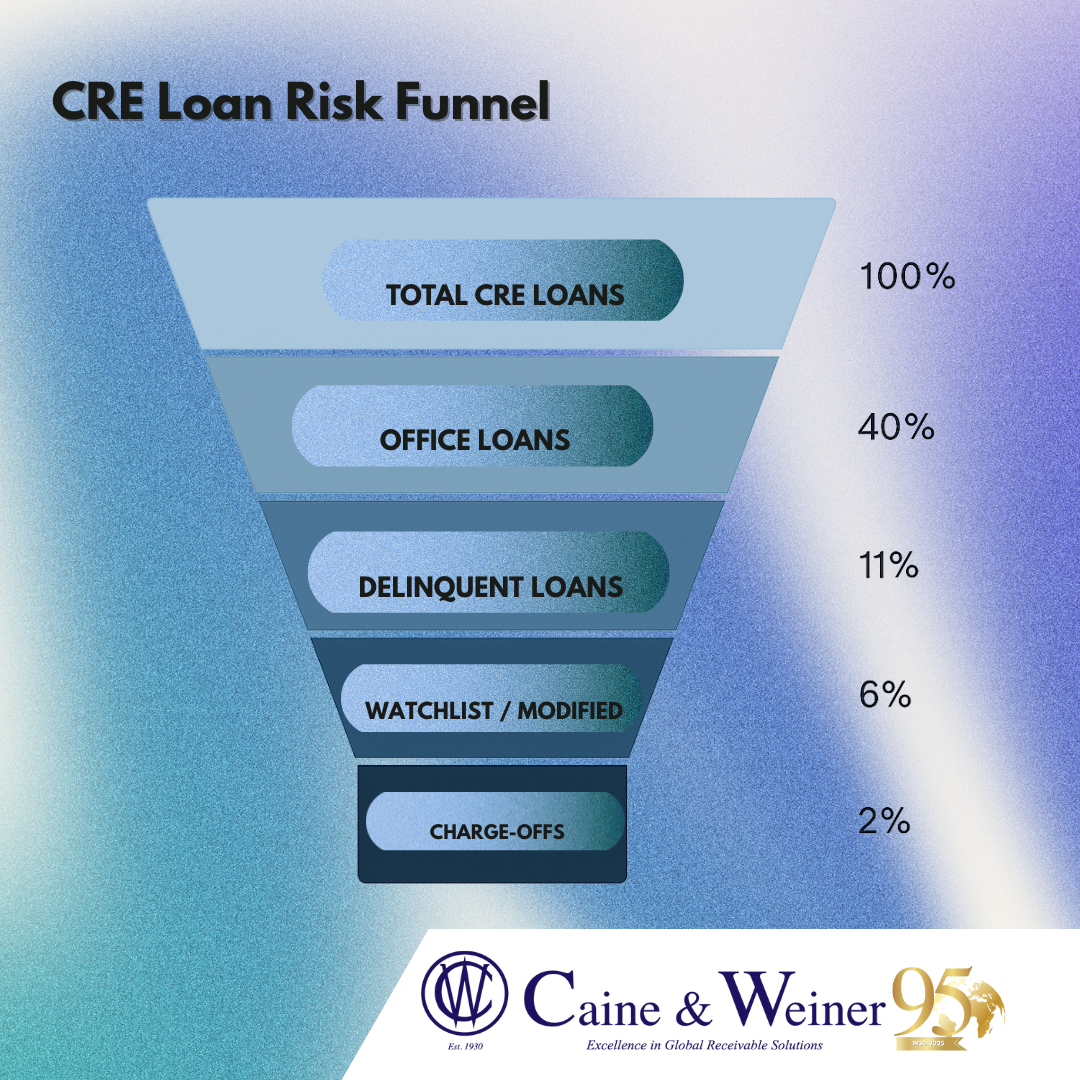

1. Office Vacancies Remain Shockingly High

Nationwide office vacancy rates remain above 20% in major cities—and much higher in some urban cores. Hybrid work is no longer a temporary trend; it’s a structural shift. Buildings purchased or financed under pre-2020 assumptions are now underperforming.

Higher vacancy = lower net operating income = higher delinquency risk.

Many office owners now face:

- reduced rental income

- shrinking reserves

- difficulty securing new tenants

- deferred maintenance

- increasing loan modification requests

This is the pressure point lenders are watching most closely.

2. Refinancing Shock Is One of the Biggest Threats to Banks

Between 2024 and 2026, more than $1 trillion in CRE loans are scheduled to mature.

This is where the crisis intensifies:

- Loans originated at 3–4% interest are refinancing at 6–8%+

- Debt-service coverage ratios are falling below renewal thresholds

- Borrowers with weak cash flow cannot qualify for new financing

- Many loans require restructuring, extensions, or capital injections

Every maturing loan is now a potential delinquency.

3. Multifamily Is Stronger—but Not Invincible

While multifamily remains resilient, it faces:

- rising operating costs

- unpredictable rent caps or local regulations

- higher insurance premiums

- increased maintenance and turnover expenses

Margins are tightening. Some markets are softening. And delinquency risk is inching upward, especially in oversupplied regions.

4. Retail & Industrial Are No Longer Guaranteed Safe Havens

Industrial was a pandemic-era star, but demand is leveling out. Retail, driven by e-commerce pressure, is stabilizing but not fully recovered.

Banks now carry broader sector risk—not just office risk.

How CRE Stress Impacts Banks Directly

1. Rising Delinquencies Strain Reserve Requirements

Banks must allocate capital based on expected losses. As delinquencies rise, reserves must rise too.

Higher reserve requirements =

✔ less capital available for lending

✔ lower earnings

✔ stricter credit standards

✔ more pressure from regulators

When CRE portfolios deteriorate, every other banking operation tightens.

2. Liquidity Tightens as Borrowers Slow Payments

Cash-flow disruptions among property owners mean:

- delayed loan payments

- increased requests for extensions

- higher charge-off probabilities

This constricts liquidity—forcing banks to reconsider lending strategies.

3. Regulatory Scrutiny Intensifies

FDIC, OCC, and Federal Reserve examiners have increased oversight of:

- CRE concentration

- underwriting practices

- stress-testing methodologies

- reserve adequacy

- workout strategies

Banks with higher CRE exposure face tougher exams and more questions.

4. Charge-Off Cycles Are Growing

Charge-offs rise when:

- borrowers enter long-term delinquency

- collateral values drop

- refinancing fails

- modification attempts fail

These losses directly impact a bank’s capital buffers and lending capacity.

Strengthening Bank Resilience Through AR Strategy

Banks cannot control the CRE market. But they can control how they manage risk, collections, and receivables.

Here are the 2025 strategies forward-thinking institutions are adopting:

1. Early Intervention: The #1 Predictor of Reduced Losses

The sooner a bank contacts a borrower, the higher the recovery rate. Banks with the lowest delinquency roll rates use:

- automated alerts

- early outreach

- segmentation by risk profile

- customized borrower engagement

- digital-first communication channels

Proactive contact prevents borrowers from disappearing into deeper delinquency.

2. Data-Driven Risk Segmentation

Not all CRE borrowers carry the same risk. Advanced analytics can now examine:

- cash flow health

- tenant mix

- lease expirations

- geographic performance

- borrower credit history

- loan-to-value trends

This allows banks to prioritize accounts most likely to default.

3. Outsourcing Delinquent Accounts Sooner

Historically, banks forwarded commercial delinquencies at 120–180 days. In today’s environment, that’s too late.

Banks seeing the strongest recovery rates now outsource at:

- 60 days for high-risk profiles

- 90 days for general commercial portfolios

- immediately for unresponsive borrowers

Earlier placement = higher recovery + lower charge-off severity.

4. Enhanced Skip-Tracing for Commercial Borrowers

Commercial contacts can be difficult to track down—especially when ownership groups restructure or dissolve.

Caine & Weiner’s skip-tracing models use:

✔ business registrations

✔ multi-agency records

✔ professional licensing

✔ digital presence

✔ affiliated business entities

✔ corporate structures

This enables banks to reach decision-makers quickly.

5. Strengthening Documentation & Communication Flows

Banks should implement:

- standardized workout templates

- stricter documentation deadlines

- digital portals for document uploads

- real-time borrower communication logs

This reduces disputes and keeps borrowers accountable.

6. Protecting Losses Through Experienced Collections Partners

Banks choose Caine & Weiner because we deliver:

- highly compliant, regulatory-aligned operations

- commercial and consumer collections expertise

- specialized financial services teams

- secure, omnichannel communication

- fast, accurate reporting and audits

In a high-risk cycle, proven collections performance is essential.

What the Future Holds for Banks & CRE

CRE Will Not Collapse—But It Will Restructure

2025 isn’t a repeat of 2008. But it is the beginning of a long, multi-year adjustment.

Expect:

- more building conversions

- more note sales

- more workouts and restructures

- continued hybrid work patterns

- new underwriting standards

- slower recovery timelines

CRE will recover—but in a different form.

Banks Will Tighten Credit Throughout 2025

Anticipate:

- stricter CRE concentration limits

- higher down payment requirements

- more conservative loan terms

- increased stress-testing

- careful portfolio diversification

Liquidity preservation will be a priority.

Receivables Precision Will Become a Competitive Advantage

In periods of financial pressure, every percentage point of improved recovery matters.

Banks that adopt:

✔ modern AR workflows

✔ earlier intervention

✔ sophisticated segmentation

✔ strong external support

…will outperform peers and protect their balance sheets more effectively.

In a nutshell,

Banks are entering a pivotal moment in the CRE cycle. Rising delinquencies, refinancing pressures, and tightened reserve requirements are reshaping financial risk across the sector.

But with strong receivables strategy—including early engagement, data-driven segmentation, and expert third-party support—banks can stabilize portfolios, mitigate losses, and stay ahead of regulatory pressures.

Caine & Weiner is committed to helping financial institutions protect their receivables through advanced collections strategies, compliant operations, and unmatched commercial recovery expertise.

In a market where every decision affects liquidity, the right receivables partner is more valuable than ever.