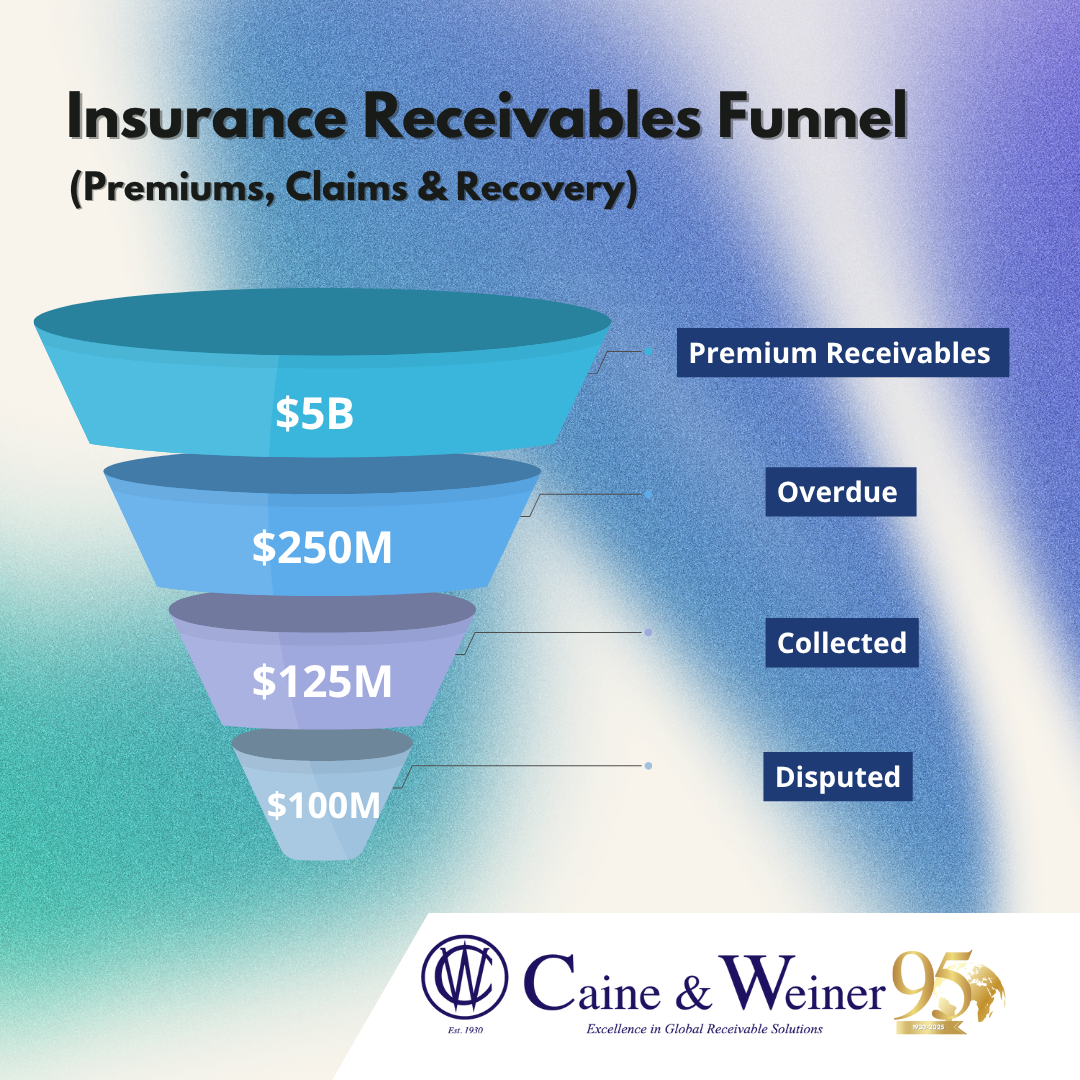

The Case of the $250 Million Delay

Imagine this: Insurer X processes $5B in annual premium receivables and holds $200M in reinsurance recoverables. A cluster of delayed payments hits — 5% of premiums are overdue by 60 days, and 2% slip into long-term disputes.

Even if half is eventually collected, the insurer faces a $250M cash flow gap, tying up working capital, delaying claims, and forcing the CFO to reallocate reserves — all while regulatory eyes are watching closely.

What looks like “just paperwork” is actually a systemic risk lever. Receivables aren’t just numbers on a ledger — they are the backbone of liquidity, capital efficiency, and risk management.

Why Receivables Matter in Insurance

Insurance may appear simple — pay a premium, get coverage. But behind every policy and claim lies a web of accounts receivable:

- Premium Receivables

- Policies issued to corporate, commercial, and consumer clients generate recurring payments.

- Lapses, delays, or non-renewals create immediate cash-flow events.

- Policies issued to corporate, commercial, and consumer clients generate recurring payments.

- Reinsurance Recovery

- Following major claims, insurers expect reimbursements from reinsurers.

- Delays or disputes here can stall payouts, pressure reserves, and distort capital planning.

- Following major claims, insurers expect reimbursements from reinsurers.

- Subrogation & Indemnification

- Post-claim, insurers pursue liable third parties.

- Legal timelines and settlement negotiations often mean these receivables linger, sometimes months.

- Post-claim, insurers pursue liable third parties.

- Intercompany Receivables

- Within multi-entity insurers, cross-line or subsidiary receivables can create internal liquidity bottlenecks.

- Within multi-entity insurers, cross-line or subsidiary receivables can create internal liquidity bottlenecks.

Side Stat: In 2022, U.S. insurers reported $982B in CRE exposure, including mortgages and CMBS. Exposure to mortgage loans alone hit $727B, ~8.9% of insurer assets (NAIC). Even minor receivables inefficiencies here can create significant capital drag.

The Multi-Dimensional Risk Landscape

- Liquidity Mismatch: Delays in premiums or recoveries disrupt claims funding, underwriting, and investments.

- Capital & Rating Sensitivity: Rating agencies track reserves and surplus. Poor receivables performance can weaken credit ratings and limit capital flexibility.

- Underwriting Feedback Loops: Weak AR discipline can lead to mispriced policies, lenient terms, and higher collections risk down the line.

- Cost & Efficiency Leaks: Manual reconciliation, dispute handling, and legal escalation inflate cost-per-dollar-collected, silently eroding margins.

Side Stat: According to APQC benchmarks, many insurers experience AR inefficiency rates above 10–15%, primarily due to aging receivables, disputes, and reconciliation delays.

Strategic Prescription: Turning Receivables Into a Competitive Advantage

The solution isn’t just chasing payments — it’s embedding receivables discipline across underwriting, claims, and finance.

1. End-to-End AR Automation

Integrate billing, reminders, dispute handling, escalations, and reconciliation into one seamless platform. It reduces delays, human error, and manual follow-ups.

2. Receivables Segmentation

Classify by risk: small commercial, large corporate, reinsurance, subrogation. Apply customized collection rules per segment.

3. Dynamic Escalation Paths

Laddered approach: reminder → negotiation → legal/external collection. Embeds accountability in policy terms where feasible.

4. Align Underwriting & Collections

Feedback loops ensure collections performance informs pricing, credit checks, and contract terms. Minimizes future delinquency risk.

5. Credit Enhancement & Insurance

Reinsurance, credit insurance, or surety bonds can offset risk in large premium portfolios or subrogation claims.

Real-World Impact

Back to Insurer X:

- With $5B in annual premium receivables, 5% overdue (≈$250M) and 2% in dispute:

- Automated resolution, predictive segmentation, and external recovery could reduce DSO, shorten payment cycles, and lower write-offs, freeing hundreds of millions in capital for growth and claims.

Without this, the opportunity cost, interest, and capital drag quietly erode profitability and flexibility.

Don’t let delayed premiums or subrogation claims disrupt your capital and cash flow. Partner with Caine & Weiner to map receivables, automate collections, and recover payments without compromising client relationships.

Contact us to strengthen your insurance receivables backbone today.