Banking and real estate are tightly interwoven. That’s never been more evident than now—when elevated commercial real estate (CRE) delinquencies are beginning to bite into core balance sheet resilience. As regulators and investors alike watch closely, banks must not treat this as a niche exposure but as a frontline risk.

In 2024–2025, banks have faced a rise in CRE noncurrent loans, especially in the office and lodging segments. The FDIC’s 2025 Risk Review singles out CRE and consumer credit deterioration as emerging credit risk areas. The Federal Reserve also noted that office loan delinquencies at large banks rose to 11.0% in Q2 2024 Federal Reserve. Let’s dig into how this pressure builds—and how banks can respond.

The Credit Stress Landscape

CRE Exposure Is Meaningful

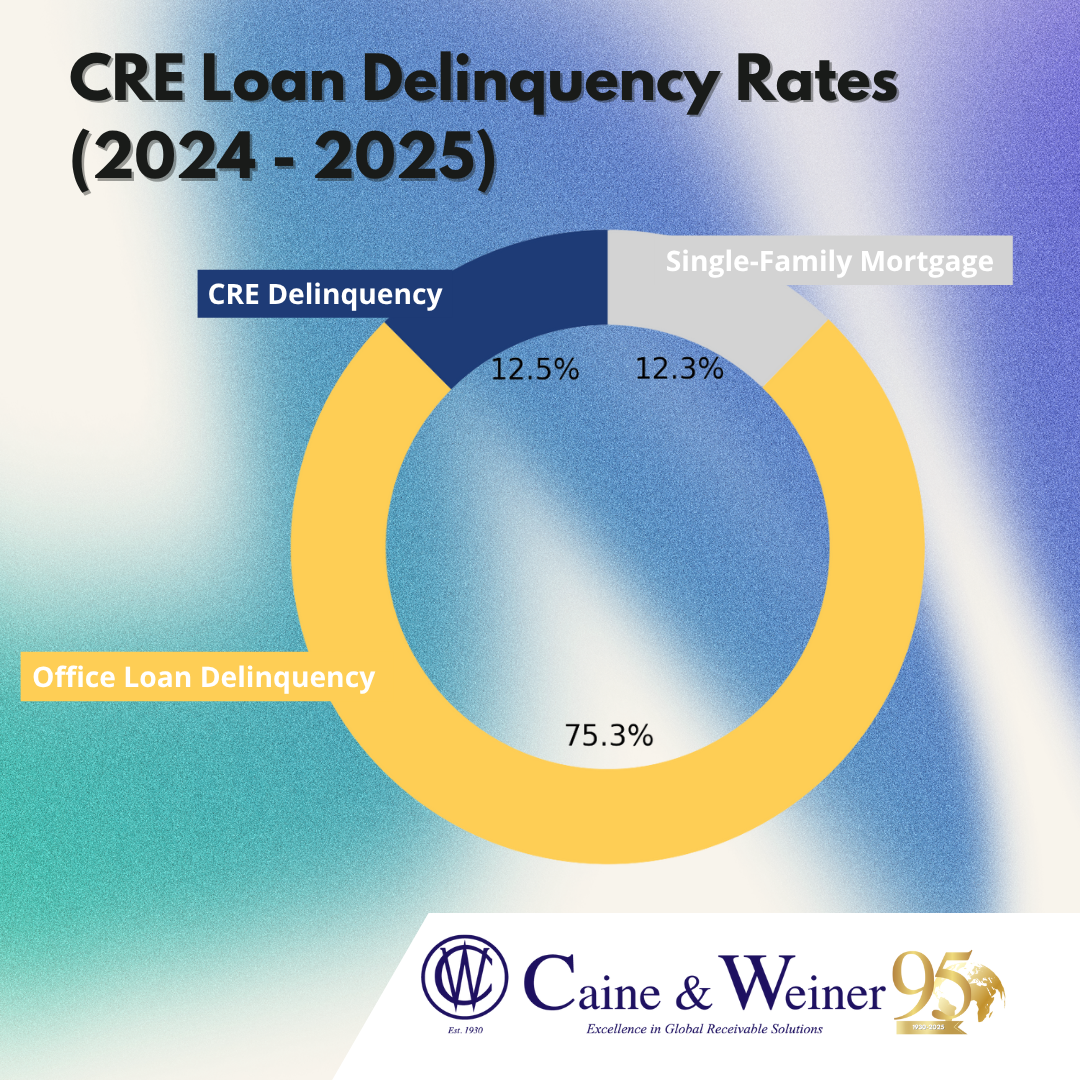

- According to CREFC MarketMetrics, bank-held CRE (30+ days) delinquency was ~1.82% in Q1 2025. crefc.org

- Office-loan hurt: in large banks, office loan delinquency rates soared to 11.0% in Q2 2024. Federal Reserve

- The GAO’s 2024 report maps how CRE strains (remote work, higher cap rates) are stressing bank portfolios. Government Accountability Office+1

- As of mid-2024, 73 banks reported delinquencies in CRE / construction / land development portfolios. Congress.gov

Broader Loan Portfolio Trends

- Delinquency rates across bank loans (loans & leases) are closely tracked by the Fed’s Charge-Off & Delinquency release. Federal Reserve

- In Q2 2025, the delinquency rate on single-family residential mortgages at U.S. banks was ~1.79%. FRED+2MacroMicro+2

- CRE is a high-leverage, slow-recovery exposure; when it goes bad, it tends to drag heavily on reserves.

Why This is a Bank’s Problem (Not Just Real Estate’s)

Reserve Erosion & Capital Stress

Banks must maintain capital against risk-weighted assets. When CRE loans go non-performing, they force provisioning, loan loss reserves, and write-downs—which hit Tier 1 capital.

Concentration Risk

Many banks, especially regional institutions, carry high CRE share in their asset mix. A shock here isn’t a blip—it’s a balance-sheet event.

Repricing & Funding Squeeze

Losses force banks to raise deposit rates or issue wholesale funding at higher spreads. That compresses net interest margin at the worst time.

Spillover & Contagion

Failures in CRE-heavy exposures may trigger MSDs (Market Sensitivity Disruptions), rating downgrades, and regulatory intervention. The losses do not remain quarantined.

Proactive Strategies for Banks

1. Portfolio Segmentation & Early Warning

Divide CRE exposure by property type, geography, lease structure, tenant stability. Deploy scorecards and leading indicators to flag stress shifts.

2. Dynamic Loss Provisioning

Move from static “coverage ratios” to forward-looking models that inject pro forma stress buffers based on macro or property-level signals.

3. Structured Workout Strategies

Arm your workout teams with playbooks: interest-only, recast, restructuring, “maturity resets,” or asset sales into special servicing.

4. Third-Party Recoveries & Receivables Approach

Adopt collections-style mindset: treat loan payments as receivables. Use escalation, monitoring, and external recoveries as part of credit discipline.

5. Diversify & Hedge

Reduce CRE concentration, hedge interest rate mismatches, and consider participations or syndications to shift risk.

Illustrative Bank Scenario

Bank A has $5B in CRE exposure, accounting for 25% of its assets. If CRE delinquency jumps from 1.0% → 3.0%, incremental impaired loans = $100M. Assume 50% is resolved or restructured; the rest becomes losses = $50M. If reserves cover $30M, capital absorbs $20M. That could reduce Tier 1 by ~2% and pressure regulatory ratios.

Scaling that across a bank’s entire portfolio, margins, and funding cost, the stress becomes existential—not just operational.

Key Takeaways & CTA

- CRE delinquencies are not orthogonal—they’re core risk for banking.

- The winners will be banks that treat troubled real estate payments as part of their “collections engine,” not anomalies.

- At Caine & Weiner, we help banks build predictive collections/servicing frameworks, design escalations, and optimize recoveries without severing client relationships.

Because in banking, tomorrow’s solvency begins with today’s receivables.