On the surface, the banking industry appears steady, structured, and predictable. Money moves in, money moves out, balances reconcile, and invoices get paid.

But talk to any vendor working with a financial institution today, and a different story emerges—one that begins not with dollars, but with delays.

It often starts with a familiar message:

“Still in approval.”

“Compliance is reviewing this.”

“Our team had a recent transition.”

Individually, these sound reasonable. But repeated over weeks—or months—they reveal something deeper: the real issue isn’t funding. Banks aren’t struggling with cash, they’re struggling with workflows.

And the data backs it up.

The Pattern Behind the Delay: A Story That Plays Out Across Banks

Let’s follow a real-world scenario—one that thousands of vendors quietly experience every year.

A vendor submits a routine invoice to a mid-sized financial institution. Nothing unusual. The bank acknowledges receipt immediately—an encouraging start.

Week 2:

“It’s with compliance.”

Week 5:

“Our approvals shifted due to a role transition.”

Week 8:

“We’re routing it for final release.”

By the time payment clears, it’s been 60, 75, sometimes even 90 days. Not because the bank is facing liquidity issues—banks maintain strong capital ratios and accessible reserves—but because the invoice became stuck in a complex, multi-layered approval chain.

This story isn’t an exception. It’s an increasingly common pattern.

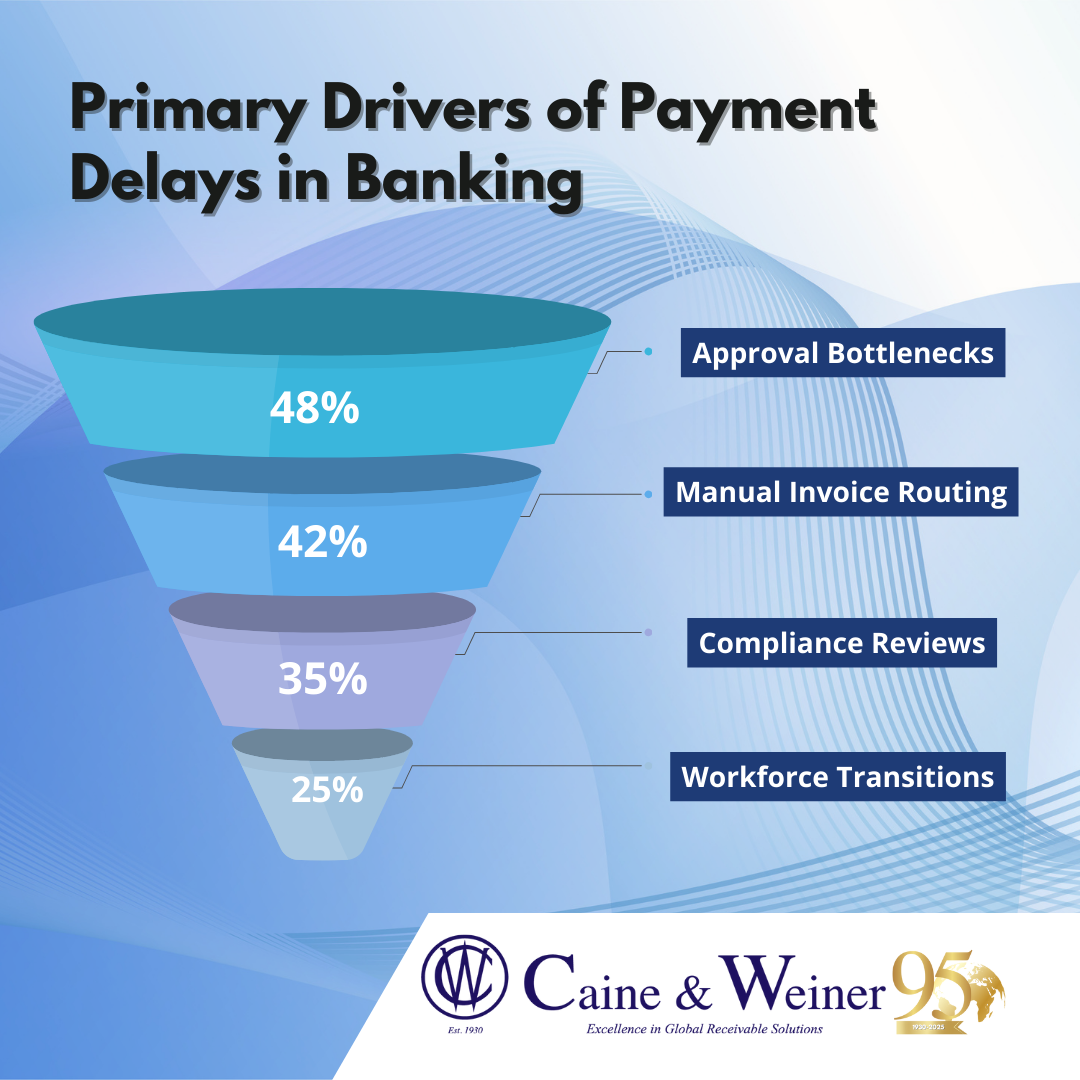

The Data: Why Workflows—Not Cash Flow—Are the Real Culprit

Across financial institutions, research now points to the same conclusion:

- Approval bottlenecks are responsible for up to 48% of payment delays in the banking sector.

Not budget constraints. Not disputes. Not vendor issues—just internal processing friction.

- Compliance requirements extend payment cycles significantly.

Banks handle more regulated workflows than nearly any other industry. Each invoice may require 3–7 approvals across operations, compliance, risk, and finance.

Every checkpoint adds time.

- Workforce transitions slow payments by 15–30%.

The banking sector experiences continual team changes—promotions, transfers, restructuring.

When roles shift, approval authority lapses—and invoices sit idle.

- Manual processes still dominate.

Even in 2025, nearly 42% of banks still rely on partially manual invoice routing, increasing the risk of stalled approvals, lost emails, or inconsistent follow-up.

- The longer the delay, the faster payment drift compounds.

Once a bank exceeds its typical payment cycle, the likelihood of crossing the next 15–30-day window increases by 2.5×.

Delays beget more delays.

The Vendor Experience: Navigating the Unknown

For vendors, late payments from banks feel paradoxical:

“How can a bank delay payment? They’re literally the financial system.”

But vendors aren’t facing a cash problem.

They’re facing a process problem.

Banks operate with caution, precision, and accountability—qualities that protect customers but inadvertently slow internal workflows.

The challenge for vendors?

You can’t see the workflow behind the delay—you only feel its effect.

So What Can Vendors Do?

While vendors cannot influence internal banking approvals, they can use strategies proven to reduce payment drift:

- Confirm the approval path early.

Understanding how many departments must review an invoice changes everything.

- Track role transitions.

New contact? New title? New routing note?

These shifts often signal upcoming delays.

- Maintain consistent but respectful follow-up.

In banking, silence is the first sign of stagnation.

- Document turnaround patterns.

Recurring patterns often reveal the true source of delays.

- Escalate based on data, not frustration.

Banks respond well to structured reminders backed by timelines—not emotion.

Caine & Weiner works with vendors across banking, fintech, and financial services to identify these patterns early and engage with professionalism, not pressure. Our goal is simple: preserve relationships while improving payment timing.

But the biggest takeaway isn’t about us—it’s about recognizing the real reason banks delay payment:

It’s not cash. It’s complexity.

And complexity can be managed—when you know what to look for.