The Bedrock Is Shifting

For decades, mining has been the economic backbone of regions across the U.S. — a sector known for its grit, capital intensity, and strategic importance. From copper that powers EVs to rare earths critical for semiconductors, mining has always felt essential.

And when something feels essential, financial risk tends to get underestimated.

But lately, the numbers are starting to tell a different story. Beneath the surface of steady commodity flows and multi-year contracts, a quiet rise in payment delinquencies is rippling through mining supply chains — from equipment leasing and fuel suppliers to contract haulers and logistics firms.

In Q2 2025, trade credit delinquencies in the U.S. mining sector rose to 5.7% — the highest level since 2016 (Experian Trade Credit Index).

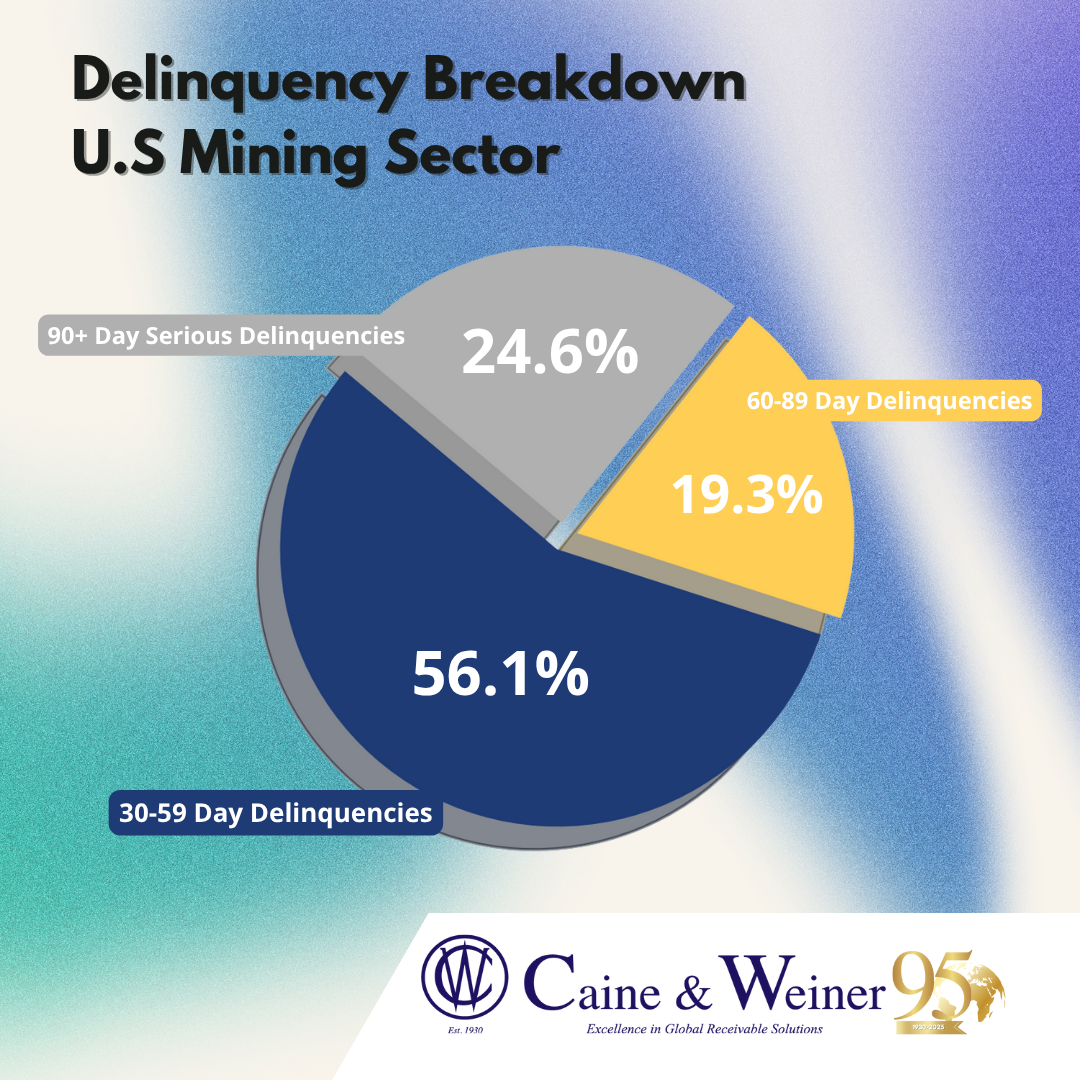

- 30–59 day delinquencies: 3.2%, up from 2.6% YoY

- 60–89 day delinquencies: 1.1%, up from 0.8% YoY

- 90+ day serious delinquencies: 1.4%, up from 0.9% YoY

While these may not sound catastrophic, remember: mining margins are notoriously cyclical. A few basis points can make or break quarterly liquidity.

What used to be shrugged off as “slow payers” is increasingly turning into real working capital drag — and in a capital-heavy sector like mining, that’s a flashing red light.

The Numbers Behind the Rock Face

Data from PayNet and CEDC reveals that supplier receivables aged 30+ days grew 21% YoY in Q2 2025, particularly in:

- Equipment leasing & maintenance contracts

- Diesel & energy supply accounts

- Specialized labor contractors for extraction & site prep

Many of these suppliers operate on thin credit lines themselves. A delayed payment from one major mine operator can cascade down the chain quickly.

Bank-Extended Credit Is Getting Riskier

Federal Reserve data (H.8 reports) shows that commercial and industrial (C&I) loan delinquency in the mining sector reached 1.84% in mid-2025, up from 1.25% a year prior.

Regional banks in mining-heavy states like Nevada, Wyoming, and West Virginia are carrying above-average exposure. Some community lenders report that 30% of their commercial loan books are tied — directly or indirectly — to resource extraction and services. When commodity prices wobble or project timelines extend, those loans age fast.

Global Headwinds Are Amplifying Local Stress

Commodity markets are notoriously global.

- Copper prices fell 8.3% between January and June 2025 (LME) amid slowing Chinese demand.

- Lithium spot prices dipped 25% YoY, pressuring newer extraction projects that were financed at peak valuations.

- And gold, while stable, has seen volatility that affects cash flow planning for mid-tier producers.

Combine price volatility with rising borrowing costs, and receivables are becoming the pressure valve for liquidity.

The Competitive Edge: Receivables Discipline

Mining has always been defined by its ability to endure cycles — but today’s delinquency uptick isn’t just another fluctuation. It’s a structural shift demanding sharper credit and collections strategies.

The companies that will navigate this environment successfully won’t just rely on operational resilience — they’ll master their receivables.

- Monitor counterparties with real-time visibility

- Segment risks before aging snowballs

- Intervene early to preserve working capital

In mining, strong cash flow is as critical as strong ore grades.

Don’t let receivables risk quietly erode your margins.

Partner with Caine & Weiner to build a smarter, faster collections framework tailored for mining.

From predictive analytics to multi-tier escalation, we help you protect working capital, stabilize cash flow, and stay ahead of the cycle.