The Call Every Banker Remembers

It usually happens on a Wednesday.

A loan officer opens their inbox to see a message flagged urgent:

“Tenant filed for bankruptcy. Cash flow disruption expected. Requesting modification.”

That single line represents exactly what banks fear—unpredictability.

In 2024–2025, those emails have become a lot more common. Office occupancy hasn’t recovered. Leasing debt is aging. Large tenants are reevaluating space. And for regional banks, CRE is no longer a quiet line item. It’s a pressure point strong enough to shake reserves.

You’ll hear bankers say: “We’ve been through cycles.”

But the data shows this one is different.

The Stress Beneath the Surface

According to the FDIC 2025 Risk Review, CRE and consumer credit are the two fastest-deteriorating portfolios in U.S. banking. And the most troubling segment?

Office loans — now at 11.0% delinquency at large banks (Federal Reserve)

Think of it this way: For every 10 office-backed loans on a major bank’s books, one is now impaired or at least sliding in that direction.

But CRE isn’t acting alone.

Add three more stressors:

- Liquidity tightening

Wholesale funding is expensive. Deposits are unstable. Net interest margins look like they’re on a diet. - Consumer credit fatigue

Cards, auto, personal loans—all show upward late-pay trends. - Small banks have big exposure

For many regional institutions: CRE = 25%–40% of total assets.

This isn’t a footnote. It’s the whole plot.

A Real Field Story: Bank Horizon

Bank Horizon isn’t real, but the scenario is based on dozens of institutions currently under watch.

They’re a mid-size regional bank with $18B in assets and a high CRE concentration. When remote work stuck longer than predicted, their office-loan book started twitching. Then shaking.

One anchor tenant downsized. Another closed regional operations. Two moved to month-to-month extensions.

Within six months:

- Office-loan delinquency rose from 1.7% to 4.9%

- Watchlist credits tripled

- Provisioning eroded income by $32M

- Risk ratings triggered regulatory review

And here’s the kicker: None of the loans had actually defaulted.

They were simply moving slower, paying late, or requesting workouts—problems of timing and cash flow, not insolvency.

Which means something important:

Banks are not losing money because borrowers are failing. They’re losing money because borrowers are failing to pay on time.

That’s receivables problem hiding in plain sight.

The Receivables Lens: What Banks Overlook

Collections is often considered a back-office activity in banking. But in today’s market? It is the highest-leverage risk-control tool they have.

Modern receivables strategies:

- identify early delinquency signals

- segment borrowers into behavioral clusters

- automate payment nudges

- personalize outreach

- escalate with precision

- recover without damaging client relationships

A TransUnion 2024 servicing study found:

Banks using modern collections systems improved repayment rates by 29% in six months. Banks using manual or reactive outreach saw charge-offs rise 18%

That’s the difference between positive earnings and a reserve bleed.

The Human Side: Why Borrowers Go Late

One CFO of a commercial borrower put it bluntly: “We’re not short on money. We’re short on organization.”

And the data agrees.

RevOps Institute (2024) found: 68% of late CRE or business payments stem from administrative delays —not distress.

Common causes:

- delayed lease renewals

- tenant rollovers

- slow AP processes

- missed emails

- outdated contact information

- accounting errors

This means banks aren’t battling insolvency—they’re battling invisibility.

The receivables advantage is simple:

1. You make the invisible visible early.

2. And act before delinquencies become defaults.

The Chain Reaction Banks Can’t Ignore

A single late CRE loan is rarely catastrophic.

But dozens? Across different segments?

That’s ripple → wave → storm.

Each late payment:

- forces higher reserves

- strains capital ratios

- pressures funding cost

- drags earnings

- spooks investors

- invites regulatory scrutiny

It’s the financial version of a slow leak in a submarine.

You don’t sink right away. But you will sink.

The New Playbook: What Banking Leaders Are Doing Now

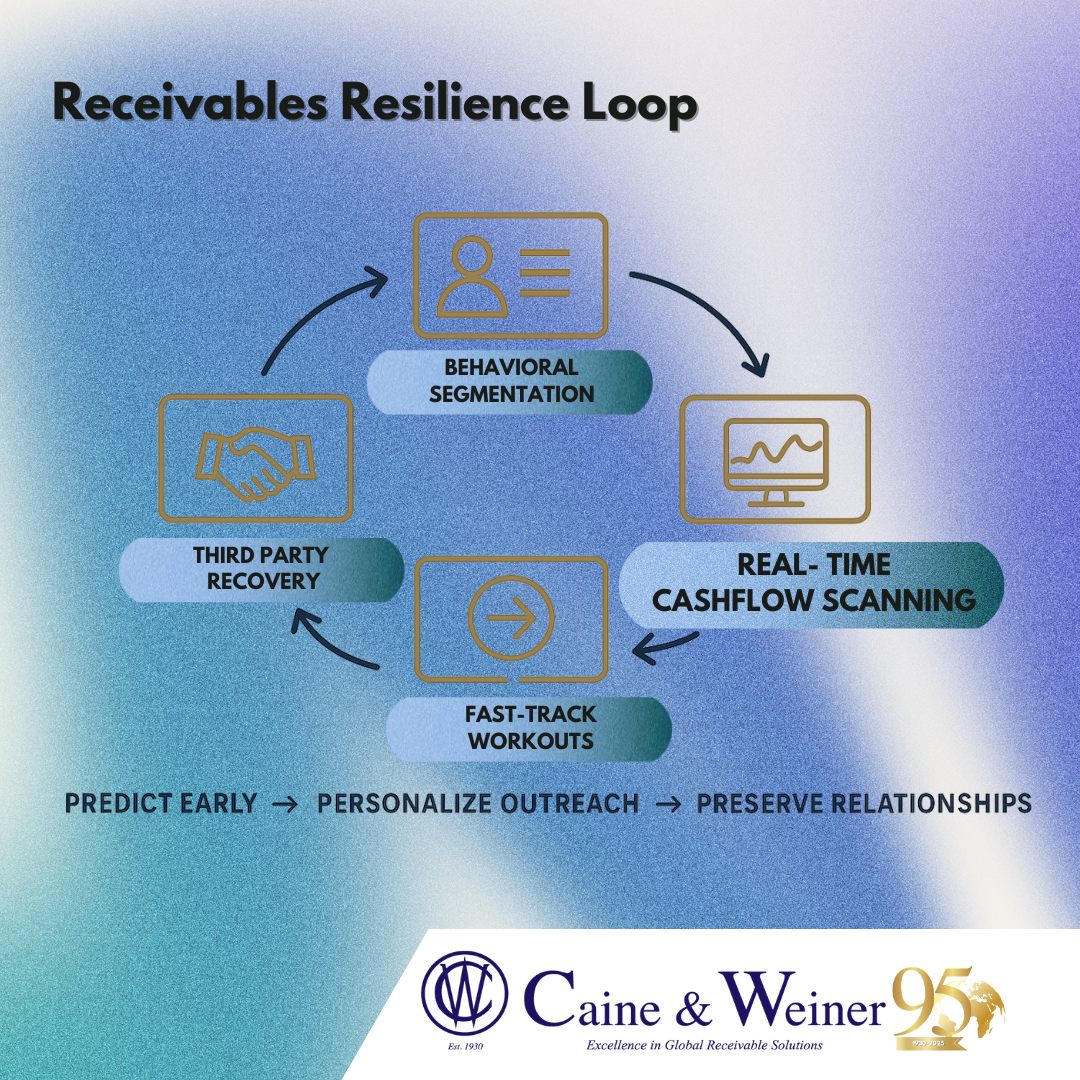

1. Behavioral Portfolio Segmentation

Using risk data + borrower behavior, banks are segmenting loans into:

- high-probability rollers

- chronic slow-payers

- silent attriters

- administrative delinquents

This allows smart escalation, not blanket pressure.

2. Real-Time Cash Flow Scanning

Banks pair payment patterns with CRE tenant-level data to predict stress before it shows up.

3. Workout Playbooks That Move Faster

Interest-only, recasts, resets, streamlined approval paths—built for speed, not paperwork.

4. Third-Party Recovery Partners (Caine & Weiner)

Banks offload slow-paying, administratively delayed, or lower-risk delinquent accounts to recovery specialists to keep cash flowing without burning relationship capital.

Caine & Weiner’s advantage: Receivables recovery with brand-safe communication.

Meaning:

You keep the relationship.

We keep the cash moving.

A Final Story: How One Bank Turned Chaos Into Strength

A community bank partnered with Caine & Weiner to modernize its receivables process across its CRE and business lending book.

6 months later, they saw:

- 32% reduction in late payments

- $18M in recovered early-stage delinquencies

- 11% improvement in capital ratio stability

- 0 lost relationships (zero customer churn)

Their CEO said:

“We realized collections isn’t about chasing money—it’s about staying ahead of problems.”

Exactly.

Bottom Line

The CRE and credit landscape is shifting faster than banks expected. But the institutions thriving today aren’t the ones with the biggest balance sheets.

They’re the ones who:

✔ predict early

✔ personalize outreach

✔ streamline recoveries

✔ protect relationships

✔ treat receivables as a core risk function, not a back-office chore

For them, tomorrow’s solvency truly begins with today’s receivables. And that’s where Caine & Weiner stands with you—turning delinquency signals into strategic advantage.