A perfect storm—rising vehicle prices, persistent inflation, elevated interest rates, softening credit approvals, and supply-chain rebalancing—has collided to reshape the financial backbone of the automotive industry. The result? Higher delinquencies, increased charge-offs, and growing pressure on accounts receivable portfolios across OEMs, lenders, and dealerships.

Caine & Weiner’s 90+ years in receivables management gives us a front-row view of this shift. And the data is clear: 2025 is the year when financial precision becomes as essential as engineering excellence.

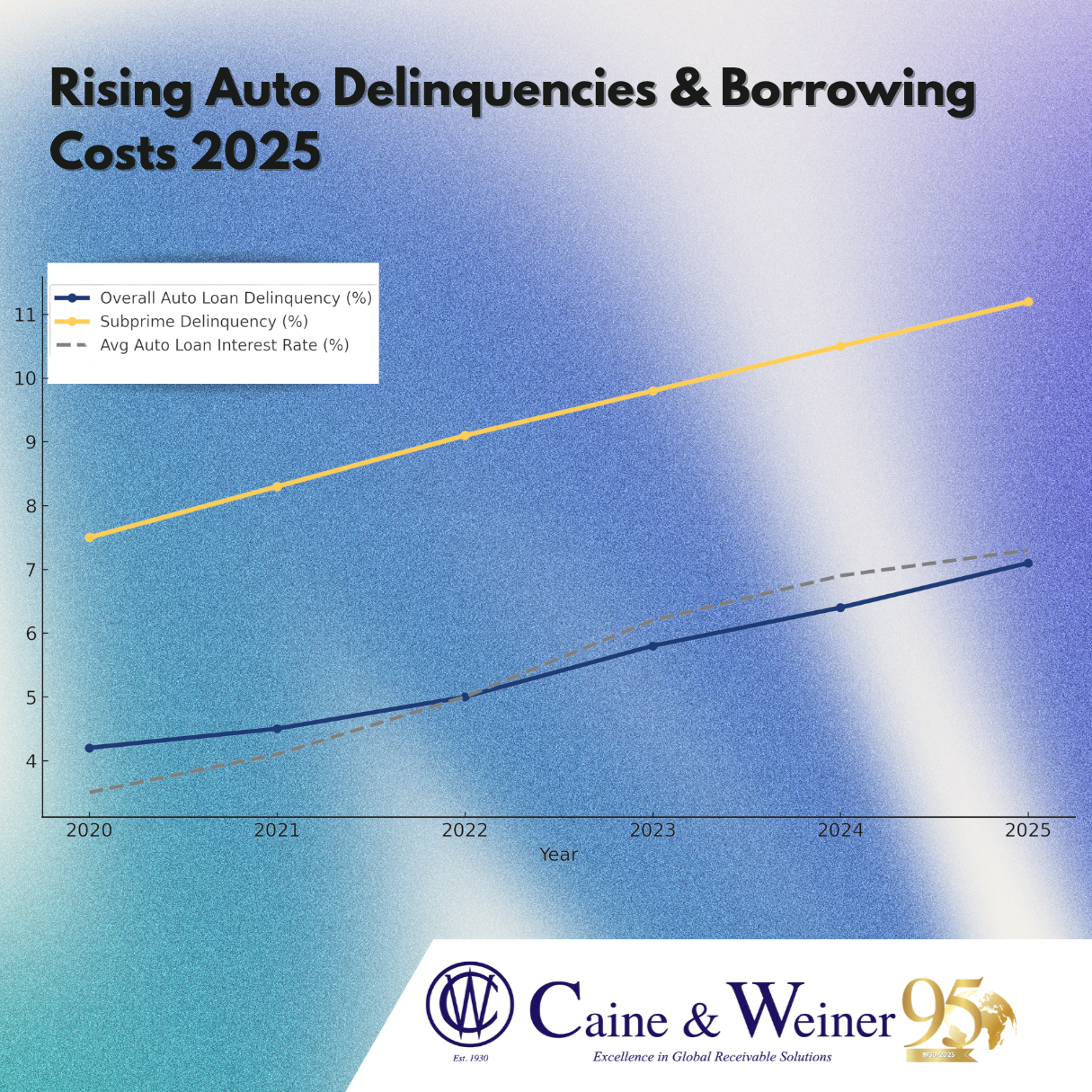

The New Financial Reality for Automotive

Affordability Has Hit a Breaking Point

The average new-vehicle price has risen over 30% in the last five years, while household income hasn’t kept pace. Combined with interest rates that remain elevated compared to pre-2020 levels, monthly payments are at historic highs.

- Larger monthly payments = higher delinquency risk

- Longer-term loans (72–84 months) = longer exposure to default

- More negative equity = lower consumer resilience

By mid-2024, 60- and 90-day delinquencies had reached decade highs, particularly among subprime borrowers. That trend continues into 2025 as lenders tighten credit, reducing approvals for riskier profiles.

Supply Chain Stabilized, But Not Costs

Although supply chains improved significantly after pandemic disruptions, elevated logistics and materials costs remain. OEMs continue to face higher production expenses, making cash-flow timing more critical than ever.

When dealers delay payments for inventory, OEMs feel the strain almost immediately.

4. EV Transition Is Another Receivables Risk Factor

Electric vehicle adoption is still growing, but not as quickly as projected in 2020–2022 forecasts. Inventory imbalances and incentive volatility contribute to unpredictable receivables cycles.

Slower turnover = tighter cash-flow windows.

Protecting Cash Flow: What Auto Companies Must Do Now

1. Strengthen Early-Stage Intervention

The most successful auto receivables teams are shifting from reactive to proactive engagement. This means:

- automated payment reminders

- faster follow-up on slow-pay accounts

- data-driven segmentation of high-risk accounts

Early outreach drastically reduces the likelihood of roll-forward delinquency.

2. Use Third-Party Collections Earlier

Traditionally, auto businesses waited until 120–180 days before outsourcing. That lag is no longer sustainable.

2025 leaders are now forwarding accounts at:

- 45 days for subprime/at-risk profiles

- 60 days for commercial service accounts

- 90 days for dealer-related balances

Accelerated placement prevents portfolio deterioration.

3. Modernize Skip-Tracing & Micro-Segmentation

With increased consumer mobility and more frequent job transitions, locating debtors requires advanced data sources.

Caine & Weiner’s data analytics tools now pull from:

✔ employment models

✔ digital footprint behavior

✔ alternative credit indicators

✔ multi-agency public records

This leads to faster contact and higher recovery.

4. Strengthen B2B Credit Controls

For dealerships and suppliers, commercial credit is becoming riskier. Protective measures include:

- updated credit applications

- uniform credit limits

- stricter documentation

- clearly defined dispute windows

- automated invoice delivery

A cleaner AR process means fewer disputes downstream.

The Path Forward: A More Resilient Automotive Finance Ecosystem

The industry is not simply facing a temporary downturn. Instead, it is entering a new financial normal built on:

- more cautious lending

- digitally empowered consumers

- higher sensitivity to price

- greater emphasis on operational efficiency

- data-driven collections practices

OEMs and dealers who modernize their receivables now will be the ones who stay competitive long-term.

What Now?

In 2025, automotive success depends on more than strong sales. It depends on efficient, disciplined, and analytics-driven receivables management.

As delinquencies rise and affordability pressures continue, cash-flow resiliency must sit at the center of every financial strategy. For OEMs, lenders, and dealers, the companies that adopt best-in-class AR practices today will be the ones steering confidently into the future.

Caine & Weiner is committed to helping automotive clients build that resilience—with the people, the platform, and the proven collections strategies to protect margin and cash flow in any market cycle.